Backdoor Bailouts Begin

The Treasury Department’s release of $100 million from the Hardest Hit Fund last week amounts to a federal bailout of five Michigan cities without congressional… Read More

The Treasury Department’s release of $100 million from the Hardest Hit Fund last week amounts to a federal bailout of five Michigan cities without congressional… Read More

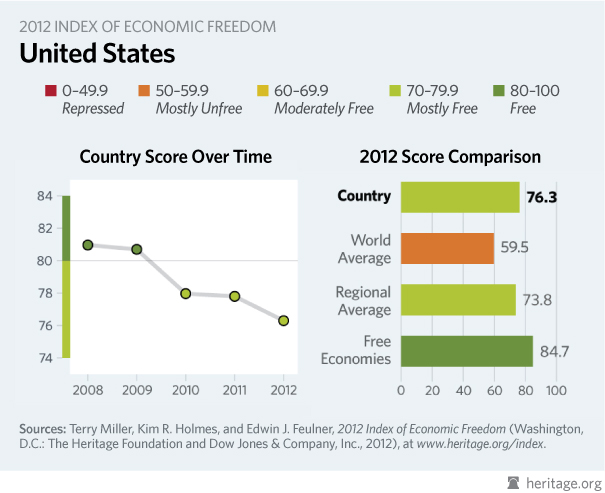

Back in 2010, The Heritage Foundation’s Index of Economic Freedom first reported the shocking erosion of America’s long-cherished economic freedom. The interventionist policies put in… Read More

There were plenty of lessons to learn after the financial crisis of 2008. Unfortunately, neither Congress nor the Obama Administration was willing to take the… Read More

House investigators are alleging a White House double standard in its rhetoric toward executive compensation for large financial institutions. The allegations appear in a report… Read More

The Small Business Lending Fund was cleverly named by its authors last Congress. Since its implementation, however, it would appear a more appropriate name would… Read More

$154 billion. That is the amount of taxpayer money that will be needed to bail out Fannie Mae and Freddie Mac according to a new… Read More

This past Friday the Associated Press reported: Nearly half of the 1.3 million homeowners who enrolled in the Obama administration’s flagship mortgage-relief program have fallen… Read More

Carnegie Mellon University economics professor and American Enterprise Institute visiting scholar Allan Meltzer has a must read op-ed in today’s Wall Street Journal titled: Why… Read More

A whopping 62 percent of Americans now say the United States is on the wrong track, yet President Barack Obama and liberals in Congress continue… Read More

On October 13, 2008, Treasury Secretary Henry Paulson summoned the CEOs of the nation’s largest banks into a gilded conference room at the Treasury Department… Read More